RECORDING OF TRANSACTION

LEARNING OBJECTIVES

- After studying this chapter, you will be able to :

- explain how to Prepare accounting vouchers;

- apply accounting equation to explain the effect of transactions;

- record transactions using rules of debit and credit;

- record transactions in journal and other subsidiary books;

Suggested Methods : Discussion method, Illustration method, Problem solving method etc.Source Document :

A document which provides evidence of the transactions is called the Source Document such as Cash memo, Invoice etc. At times, there may be no documentary proof for certain items in such case voucher may be prepared showing the necessary details and it must be approved by appropriate authority. All recording in books of account is done on the basis of Voucher.

Classification of Accounting Vouchers :

| Vouchers | Further classification | Purpose |

Cash Vouchers | Debit Vouchers

Credit Vouchers | To show Cash Payments

To show Cash Receipts |

| Non Cash Vouchers | Transfer Vouchers | To show Transactions not involving cash |

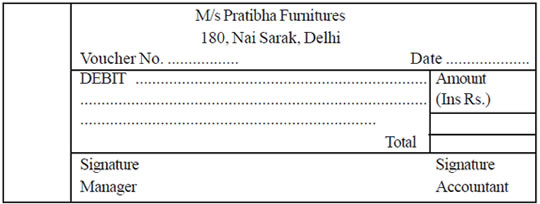

Debit Voucher :

This voucher is prepared for all the cash payments made by the business e.g. Payment of Salary, Purchses of Goods and services, Payment made to any Creditor etc.

Format of Debit Voucher

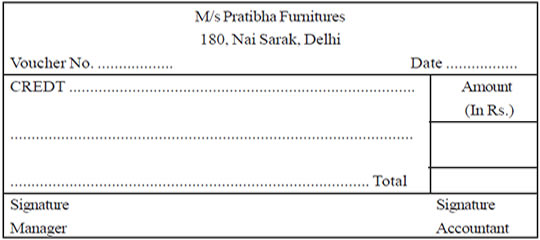

Credit Voucher :

This voucher is prepared by the business in case of cash receipt from any source such as Sale of goods for Cash, Payment received from any of Debtors, Income received etc.

Format of Credit Voucher

Transfer Voucher / Non-Cash Voucher :

This type of vouchers are prepared in those transactions which do not involve Cash. Such as Credit Sales, Credit Purchases, Bad Debts, Depreciation charged etc.

Format of Transfer Voucher

ACCOUNTING EQUATION

An accounting equation is based on the dual concept of accounting. According to this concept every transaction has two aspects - Debit and Credit.

Assets = Capital + Liabilities

A transaction may affect either both sides of the equation by the same amount or one side of the equation only, by both increasing or decreasing it by equal amount. It can be said "Accounting equation holds good under all circumstances."

1. Analysis of Business Transactions :

A. Commenced business with Cash Rs. 2,00,000.

This transactions will affect the assets as the firm is receiving asset in the form of Cash and the owner of the business has invested amount, this will affect the Capital of the business

| ASSETS | = | CAPITAL + LIABILITIES |

| Cash | | |

| Transaction | 2,00,000 | = | 2,00,000 + 0 |

B. Bought goods from Ram Rs. 25,000.

This transaction will affect both assets as well as liabilities of the business. The goods and Creditors are increasing.

| ASSETS | | = | CAPITAL + LIABILITIES |

| Cash |

Goods

| | | Creditors |

| Old Equation | 2,00,000 | | = | 2,00,000 | + 0 |

| Transactions | 0 |

+ 25,000

| |

0

|

+ 25,000

|

| New Eq. | 2,00,000 + 25,000 | = | 2,00,000 | + 25,000 |

2. Transactions affecting only assets side of the equation :

A. Bought goods for Cash Rs. 35,000

This transaction will affect the Cash and Goods by Rs. 35,000. the firm is paying the money resulting in decrease of Cash. Goods are increasing.

| ASSETS | | = | CAPITAL + LIABILITIES |

| Cash | Goods | | | Creditors |

| Old Equation | 2,00,000 + 25,000 | = | 2,00,000 | +25,000 |

| Transaction | –35,000 + 35,000 | |

0

|

+ 0

|

| New Eq. | 1,65,000 + 60,000 | = | 2,00,000 | + 25,000 |

B. Bought Furniture for cash Rs. 50,000

This transactions has brought about two changes in the assets side only. One asset i.e. Cash is decreasing and other asset i.e. Furniture is increasing.

| ASSETS | | | = |

CAPITAL + LIABILITIES

|

| Cash | Goods | Furniture | | | | Creditors |

| Old Equation | 1,65,000 + 60,000 | | = |

2,00,000

| +25,000 |

| Transaction | –50,000 + 0 | + 50,000 | |

0

|

+

|

0

|

| New Eq. | 1,15,000 + 60,000 | + 50,000 | = |

2,00,000

| + 25,000 |

3. Transactions affecting only liabilities side of the equation

A. Accepted a bill drawn by Ram for Rs. 25,000 for 3 months.

This transaction will affect Creditors and Bills Payable. As one liability i.e. Creditor is decreasing and other liability i.e. Bills payable is increasing.

| ASSETS | | = | CAPITAL + LIABILITIES | |

| Cash | Goods | Furniture | | Creditors + B/P |

| Old Equation | 1,15,000 + 60,000 | + 50,000 | = | 2,00,000 + 25,000 |

| Transaction | 0 |

+

|

0

| + |

0

| = |

– 25,000 + 25,000

|

| New Eq. | 1,15,000 + 60,000 | + 50,000 | = | 2,00,000 + 0 |

+ 25,000

|

4. Transaction affecting the Capital only

A. Interest on Capital provided Rs. 2000

| ASSETS | |

=

| CAPITAL + LIABILITIES | | | |

| |

Cash

|

Goods

| Furniture | |

Creditors + B/P

|

| Old Equation |

1,15,000 +

| 60,000 + 50,000 |

=

| 2,00,000 + 0 + 25,000 |

| Transaction | |

0

|

+

|

0

| + |

0

|

=

| – 2000 | | | |

| | | | | | | | + 2000 | | | |

| New Eq. | 1,15,000 + 60,000 | + 50,000 |

=

| 2,00,000 + 0 + 25,000 |

B. Interest on Drawings charged Rs. 1000

| ASSETS | | | | |

=

| CAPITAL + LIABILITIES |

| |

Cash

|

Goods

| Furniture | | Creditors + B/P |

| Old Equation |

1,15,000 +

| 60,000 + 50,000 |

=

| 2,00,000 |

+

|

0

|

+ 25000

|

| Transaction | |

0

|

+

|

0

| + 0 |

=

| – 1000 | | | |

| | | | | | | | + 1000 | | | |

| New Eq. | |

1,15,000 +

| 60,000 |

+ 50,000 =

| 2,00,000 |

+

|

0

|

+ 25,000

|

In the above transactions, Capital is increasing and decreasing at the same time. It is owner's duty to pay all the expenses and it is the owner who takes all the profits arising out of business.

5. Transactions related to Expenses

A. Salary Paid Rs. 5000

| ASSETS | | = CAPITAL + LIABILITIES | |

| Cash | Goods | Furniture | | Creditors + B/P |

| Old Equation | 1,15,000 + 60,000 + 50,000 |

=

| 2,00,000 |

+ 0

|

+ 25,000

|

| Transaction | – 5000 | | |

=

| – 5000 | | |

| New Eq. | 1,10,000 + 60,000 + 50,000 |

=

| 1,95,000 |

+ 0

|

+ 25,000

|

This transaction affects cash and capital because Cash is decreasing and Capital (Owner) is responsible to pay all the expenses.

6. Transactions related to Income

| A. Commission Received | Rs. 2000 | | | | |

| ASSETS | | = CAPITAL + LIABILITIES | |

| Cash | Goods | Furniture | | Creditors + B/P |

| Old Equation | 110000 + 60000 |

+ 50,000

|

=

| 200,000 |

+ 0

|

+ 25000

|

| Transactions | + 2000 | | |

=

| + 2000 | | |

| New Eq. | 112000 + 60000 |

+ 50,000

|

=

| 197,000 |

+ 0

|

+ 25000

|

This transaction affects cash and capital because Cash is increasing and Capital (Owner) is rightful for every income.

RULES OF DEBIT AND CREDIT

TRADITIONAL APPROACH

Under this approach, all ledger accounts are mainly classified into two categories:

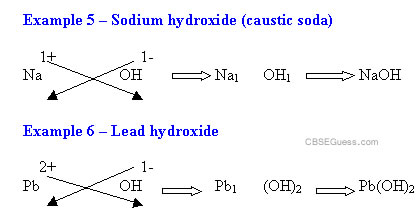

A. Personal accounts : It includes all those accounts which are related to any person i.e. individuals, firms, companies, Banks etc. This can further be classified into three categories :

1. Natural persons : All accounts of human eings/persons are included such as Ram's a/c, Shyam's a/c etc.

2. Artificial persons : This includes all accounts related to organizations which are treated as persons in the eyes of law and having all the legal rights as a natural person have such as buying/selling assets in its name, suing and be sued etc.Some of the examples are Reliance industries ltd. Punjab National Bank etc.

3. Representative persons : In this category, accounts which represents some person are included e.g. Capital a/c (representing Owner), Outstanding salary (representing the employee to whom salary is due) etc.

B. Impersonal accounts : all ledger accounts which are not related to persons are included in this category. This can be classified as :

1. Real accounts : under this category, mainly assets (excluding debtors) are included. These assets can be tangible (which can be touched, seen and measured such as furniture, cash, stock etc.) and intangible (which can't be seen, touched or measured but still have monetary value such as patents, trademark etc.)

2. Nominal accounts : all this, all accounts which are related to income/gain and expenses/losses are included e.g. Salary paid, Commission received etc.

RULES OF DEBIT/CREDIT UNDER TRADITIONALAPPROACH :

| CLASSIFICATION OF ACCOUNTS | RULES OF DR/CR |

| 1. | NATURAL PERSONS | | |

| PERSONAL | 2. | ARTIFICIAL PERSONS | DR | THE RECEIVER |

| 3. | REPRESENTATIVE | | |

| IMPERSONAL | | PERSONS | CR | THE GIVER |

| REAL | 1. | TANGIBLE` | DR | WHAT COMES IN |

| 2. | INTANGIBLE | CR | WHAT GOES OUT |

| NOMINAL | 1 | EXPENSES/LOSSES | DR | EXP/LOSSES |

| 3. | INCOME/GAINS | CR | INCOME/GAINS |

Illustrations 1: Analyse the following transactions by using the “TRADITIONAL APPROACH”

| 2011 | |

Amount (in Rs.)

|

| Jan 1 | Prateek started business with cash |

1,00,000

|

| Jan 5 | Bought goods for Cash | 20,000 |

| Jan 7 | Bought goods from Pravesh | 10,000 |

| Jan 10 | Sold goods for cash | 5,000 |

| Jan 12 | Sold goods to Vikas | 12,000 |

| Jan 15 | Paid Salary | 5,000 |

| Jan 20 | Received Commission | 2,000 |

Solution :

Analysis of Transactions

| S. no. | Transaction | Accounts Affected | Nature of Accounts | Changes | Debit (Rs.)

| Credit (Rs.)

|

| 1. | Commenced business | Cash | Real | Comes in |

1,00,000

| |

| | Capital | Personal | Giver | |

1,00,000

|

| 2. | Purchased goods | Purchases | Nominal | Expenses |

20,000

| |

| | Cash | Real | Goes out | |

20,000

|

| 3. | Bought goods on | Purchases | Nominal | Expenses |

10,000

| |

| credit | Pravesh | Personal | Giver | |

10,000

|

| 4. | Sold goods for cash | Cash | Real | Comes in | 5,000 | |

| | | Sales | Nominal | Income | | 5,000 |

| 5. | Sold goods on Credit | Vikas | Personal | Receiver | 12,000 | |

| | | Sales | Nominal | Income | | 12,000 |

| 6. | Paid Salary | Salary | Nominal | Expenses | 5,000 | |

| | | Cash | Real | Goes Out | | 5,000 |

| 7. | Received | Cash | Real | Comes in | 2,000 | |

| Commission | Commission | Nominal | Income | |

2,000

|

RULES OF DEBIT/CREDIT UNDER MODERN APPROACH :

| Assets/Expenss | Capital/lLiabilities/Revenue |

| Increase | Decrease | Increase | Decrease |

| Debit | Credit | Credit | Debit |

Illustration 2 : Analyse the transactions given in Illustration 1 by using the

"MODERN APPROACH"

Solution :

| S. no. | Transaction | Accounts Affected | Nature of Accounts | Changes |

Debit (Rs.)

| Credit (Rs.) |

| 1. | Commenced Business | Cash | Asset | Increase |

1,00,000

| |

| | Capital | Capital | Increase | |

1,00,000

|

| 2. | Purchased goods | Purchases | Expenses | Increase |

20,000

| |

| | Cash | Asset | Decrease | |

20,000

|

| 3. | Bought goods on | Purchases | Expenses | Increase |

10,000

| |

| credit | Pravesh | Liabilities | Increase | |

10,000

|

| 4. | Sold goods for cash | Cash | Assets | Increase |

5,000

| |

| | Sales | Income | Increase | |

5,000

|

| 5. | Sold goods on Credit | Vikas | Assets | Increase |

12,000

| |

| | Sales | Income | Increase | |

12,000

|

| 6. | Paid Salary | Salary | Expenses | Increase |

5,000

| |

| | Cash | Assets | Decrease | |

5,000

|

| 7. | Received | Cash | Assets | Increase |

2,000

| |

| Commission | Comm-ission | Income | Increase | |

2,000

|

JOURNAL

Journal is a book in which transactions are originally recorded in a chronological order (as per the occurance) after analyzing the transaction and applying the rules of debit and credit.

PROCESS OF RECORDING

1. Identification of financial transactions

2. Analysis of tansactions

3. Application of rules of debit and credit

4. Recording in Journal

Illustration 3 : By using illustration 1, record the transactions in Journal.

JOURNAL

| Date | Particulars | | L.F. |

Debit (Rs.)

|

Credit (Rs.)

|

| 2011 | | |

| | |

| Jan 1 | Cash a/c

To Capital a/c | Dr.

|

1,00,000

| |

| |

1,00,000

|

| (Being business commenced) | | |

| Jan 5 | Purchases a/c

To Cash a/c | Dr.

|

20,000

| |

| |

20,000

|

| (Being goods bought for cash) | | |

| Jan 7 | Purchases a/c | Dr. |

10,000

| |

| To Pravesh’s a/c

(Being goods bought on credit) | |

10,000

|

| |

| Jan 10 | Cash a/c

To Sales a/c | Dr.

|

5,000

| |

| |

5,000

|

| (Being goods sold for cash) | | |

| Jan 12 | Vikas’s a/c

To Sales a/c | Dr.

|

12,000

| |

| |

12,000

|

| (Being goods sold on credit) | | |

| Jan 15 | Salary a/c | Dr. |

5,000

| |

| To Cash a/c

(Being salary paid) |

| |

5,000

|

| |

| Jan 20 | Cash a/c | Dr. |

2,000

| |

| To Commission a/c

(Being Commission received) | |

2,000

|

|

Simple Entries : The entries in which only two accounts are affected, one a/c is debited and other one is credited. All entries in the above illustration 3 are this nature.

Compound Entries : The entries in which there are at least two accounts are debited and at least one account is credited or vice versa.

Example 1 Received Rs. 3,900 from Ram in full settlement of a claim of Rs. 4,000.

| Cash a/c | Dr. |

3,900

|

| Discount allowed a/c | Dr. |

100

|

| To Ram | |

4,000

|

(Being cash received in full settlement)

Example 2 Paid Rs. 4,900 to Shyam in full settlement who owes us Rs. 5,000.

| Shyam’s a/c | Dr. |

5,000

|

| To Cash a/c | |

4,900

|

| To Discount received a/c |

100

|

(Being Cash paid in full settlement)

SPECIAL TRANSACTIONS RELATED TO GOODS

1.

| Withdrawal of goods by owner for personal use. |

| Drawings a/c | Dr. |

| To Purchases a/c | |

2.

| Goods given as charity. | |

| Charity a/c | Dr. |

| To Purchases a/c | |

3.

| Goods distributed as free samples |

| Advertisement a/c | Dr. |

| To Purchases a/c | |

4.

| Goods lost by fire/ flood/theft etc. |

| Loss by fire/theft a/c To Purchases a/c | Dr. |

Note : Purchases a/c is credited in the above entries because the goods are going out of our business on cost and it is not a sale hence, deducted from the purchases a/c.

TRANSACTIONS RELATED BANKS :

| 1. | Cash deposited into the bank |

| Bank a/c | Dr. | |

| To Cash a/c | |

| 2. | Cash withdrawn for office use. |

| Cash a/c | Dr. | |

| To Bank a/c | |

|

| 3. | When cheque is received from customer and deposited into bank same day. |

| Bank a/c | Dr. | |

| To Customer’s personal a/c | |

| 4. | When cheque is received from customer and not deposited into bank same day. |

| Cash a/c | Dr. | |

| To Customer’s personal a/c | |

| 5. | When above cheque (Point 4) is deposited later into bank. |

| Bank a/c | Dr. | |

| To Cash a/c | | |

| 6. | When payment is made through cheque. |

| Personal a/c | Dr. | |

| To Bank a/c | | |

| 7. | When expenses is paid through cheque. |

| Expense a/c | Dr. | |

| To Bank a/c | | |

| 8. | When interest is allowed by the bank. |

| Bank a/c | Dr. | |

| To Interest a/c | | |

| 9. | When Bank charges for the services provided. |

| Bank Charges a/c | Dr. | |

| To Bank a/c | | |

Some special entries :

| 1. | Bad Debts (when customer is declared insolvent and amount is irrecoverable |

| from him) | | |

| Cash a/c | Dr. | (If partial amount is recovered) |

| Bad Debts a/c | Dr. | (the irrecoverable part) |

| To Personal a/c | | (the due amount) |

| 2. | Bad debts recovered earlier written off as bad debts. |

| Cash a/c | Dr. | |

| To Bad debts recovered a/c | |

| 3. | Outstanding Expenses (expenses due but not paid yet). |

| | Expenses a/c | Dr. | |

| To Outstanding Expenses a/c | |

| 4. | Prepaid Expenses (Expenses not due but paid in advance). | |

| Prepaid expenses a/c | Dr. |

| To Expenses a/c | |

5.

| Accrued income (income due but not received yet). |

| Accrued Income a/c | Dr. |

| To Income a/c | |

6.

| Unearned Income (Income not due but received in advance). |

| Income a/c | Dr. |

| To Unearned Income a/c |

7.

| Depreciation provided on fixed assets. |

| Depreciation a/c | Dr. |

| To Related asset’s a/c | |

8.

| Interest on Capital provided. |

| Interest on capital a/c | Dr. |

| To Capital a/c | |

9.

| Interest on Drawings charged. |

| Drawings a/c | Dr. |

| To Interest on Drawings a/c |

BOOKS OF ORIGINAL ENTRY/SPECIAL PURPOSE BOOKS

As size of the business grows and number of transactions increases, it becomes necessary for the business to divide the recording work. The books maintained are illustrated below :

| Tansactions | Further classification | subsidiary Books Maintained |

Cash & Bank Related

Transactions

| Only Cash Transactions

Cash & Bank Transactions

Cash payment of small amount | Simple Cash Book

Double Column Cash book

Petty Cash Book |

Transactions Other

than Cash & Bank

| Credit Sale

Credit Purchases

Sales Returns

Purchases Returns

Transactions of Bill receivable

Transactions of Bill Payable

Any other transaction | Sales Book

Purchases Book

Sales returns Book

Purchases Returns Book

Bill Receivable Book

Bill Payable Book

Journal Proper |

ADVANTAGES OF MAINTAINING SUBSIDIARY BOOKS :

- Division of work

- Leads to Specialization

- Easy to maintain Ledger

- Check on frauds

- Easy to fix responsibility

- Quick availability of Required information.

CASH BOOK :

Cash book shows all the transactions related to cash receipts and payments. Cash book serves two purposes. First, all the cash transactions are recorded first time in cash book it becomes BOOK OF ORIGINAL ENTRY. Second, there is no need to prepare Cash a/c in ledger it also play the role of Principal Book.

Simple Cash Book :

All the cash receipts are shown in left hand side i.e. Debit side and all the cash payments are shown in right hand side i.e. Credit side.

Points to Remember :

- Cash in hand/opening balance of cash is shown in Dr. side of the Cash book as "to Bal b/d".

- Only transactions of cash receipts and payments are recorded in this book.

- This book never show a credit balance because one can't pay more than the cash one have.

- Illustrations 4

Enter the following transactions in a Simple Cash Book :

| 2011 | |  | 2011 | |

|

| Jan. 1 | Cash in Hand | 12,000 | Jan. 5 | Received from Ram |

3,000

|

| Jan. 7 | Paid rent | 300 | Jan. 8 | Sold goods |

3,000

|

| Jan.10 | Paid to Shyam | 7,000 | Jan. 15 Purchased goods | |

| | | | from Mohan | 5,000 |

| Jan. 27 | Purchased | 2,000 | Jan. 31 Paid Salaries |

1,000

|

| furniture | | | | |

Solution :

In the Books of...

CASH BOOK

| Dr. | Receipts | | | Payments | | Cr. |

Date

2011 | Particulars | L.F. |

| Date

2011 | Particulars | L.F. |

|

|

| | |

| |

Jan. 1

Jan. 5

Jan. 8

Feb. 1 | To Balance b/d

To Ram

To Sales A/c

To Balance b/d |

12,000

3,000

3,000

| Jan. 7

Jan.10

Jan. 27

Jan. 31

Jan. 31

| By Rent A/c

By Shyam

By Furniture A/c

By Salaries A/c

By Balance c/d

|

300

7,000

2,000

1,000

7,700

|

18,000

|

18,000

|

7,700 | |

Notes : One can draw the following conclusions :

- In a Simple Cash Book only cash receipts and cash payments are recorded. Credit transactions are not recorded. Purchase from Mohan of j 5,000 on 15th Jan is a credit purchase hence, is not recorded in the Cash Book.

- The debit side is always bigger than the credit side since the payments can never exceed the available cash. This is true even for daily balances.

- It is like an ordinary account.

Cash book with Bank column

A two column cash book enable the management to know the cash and bank

balance instantly. In this book, amount column is divided into Cash and Bank columns.

| Dr. | FORMAT OF DOUBLE COLUMN CASH BOOK | Cr. |

| Date | Particulars V.N. L.F. Cash Bank Receipts side | Date Particulars V.N.L.F Cash Bank Payments side |

Points to Remember

- Bank column can show a credit balance as banks give overdraft facility to its reputed customers.

- If there is an overdraft or credit bank balance "By Bal b/d" will be shown in bank column in credit side.

- If bank balance increases, the bank column is debited and if decreases bank column is credited.

Some Special entries Contra entries :

If both cash and bank columns are affected by any transaction, it is called a contra entry. To indicate contra entry "C" is mentioned in the L.F. column.

July 5 Cash deposited into bank Rs. 5,000

| Dr. | Cash Book (Extract) | Cr. |

| | | |

| Date | Particulars | V.N. L.F. | Cash Bank Date | Particulars | V.N.L.F Cash Bank |

| July 5 | To Cash | C | 5,000 July 5 By Bank | C 5,000 |

As bank balance is increasing bank column is debited and cash balance is decreasing, cash column is credited in the above entry.

July 7 Withdrawn from Bank for office use Rs. 2,000

| Dr. | | | Cash Book (Extract) | |

Cr.

|

| | | | |

| Date | Particulars V.N. L.F | Cash | Bank Date Particulars V.N. L.F |

Cash Bank

|

| July 7 | To Bank | C | 2,000 | July 7 By Cash | C |

2,000

|

As cash balance is increasing so it is debited because of withdrawal of money bank balance is decreasing hence credited.

Treatment of cheques received from customers under different situations

1. If there is no information about the disposal of received cheque.

July 1 Received a cheque from Anu Rs. 2,500

| Dr. | | | | Cash Book (Extract) | Cr. |

| | | | |

| Date | Particulars | V.N. L.F. |

Cash Bank Date

| Particular | V.N. L.F Cash Bank |

| July 1 | To Anu | | |

2,500

| | |

When there is no information given in question, it is considered that the cheque has been deposited into bank the same day it is received.

2. When received cheque is deposited into bank later.

July 1 Received a cheque from Anu Rs. 2500

July 3 Anu's cheque deposited into bank.

| Dr. | | | Cash Book (Extract) | |

Cr.

|

| | | | | |

| Date | Particulars | V.N. L.F. |

Cash Bank Date

|

Particular V.N. L.F Cash Bank

|

| July 1 | To Anu | |

2,500

| July 3 By Bank | C |

2,500

|

| July 3 | To Cash | C |

2,500

| | | | |

When cheque is not deposited into Bank same day, it is considered as Cash. When the received cheque is deposited at later date, it will be considered as cash being deposited into bank hence contra entry has been passed.

3. If cheque is endorsed in favour of creditor of business.

July 1 Received a cheque from Anu Rs. 2,500

July 3 Anu's cheque endorsed in favour of Ram

| Cash Book (Extract) |

| Dr. | | | |

Cr.

|

| Date | Particulars |

V.N. L.F. Cash Bank

|

Date Particular V.N. L.F Cash Bank

|

| July 1 | To Anu |

2,500

| July 3 By Ram |

2,500

|

Anu's cheque is being treated as Cash hence it is considered that Cash given to Ram.

4. When cheque is dishonoured due to any reason.

July 1 Received a cheque from Anu Rs. 2,500

July 3 Anu's cheque dishonoured

Cash Book (Extract)

Dr. Cr.

Date Particulars V.N. L.F. Cash Bank Date Particular V.N.L.F Cash Bank

July 1 To Anu 2,500 July 3 By Anu 2,500

The effect of dishonour : Anu is again considered as Debtor and bank balance

decreases hence bank balance is credited.Illustration 4 : Prepare a Cash book with Bank column from the following information :

| 2011 | | |

| Jan. 1 | Cash in hand |

12,000

|

| Jan. 1 | Bank Overdraft |

3,000

|

| Jan. 5 | Deposited into Bank |

2,000

|

| Jan. 7 | Received a cheque from Pujan |

10,000

|

| Jan. 10 | Goods sold for cash |

6,000

|

| Jan. 12 | Sold goods to Naveen |

7,000

|

| Jan. 15 | Received a Cheque from Naveen |

7,000

|

| Jan. 20 | Salary paid by cheque |

5,000

|

| Jan. 21 | Naveen’s cheque deposited into bank | |

| Jan. 25 | Payment made to Shyam by cheque |

2,000

|

| Jan. 30 | Bank charged interest on overdraft |

100

|

Double Column Cash Book :

| Date | Particulars | V.N. | L.F. |

Cash

|

Bank

| Date | Particular | V.N. | L.F. |

Cash

|

Bank

|

2011

Jan. 1

Jan. 5

Jan. 7

Jan. 10

Jan. 15

Jan. 21

|

To Bal b/d

To Cash

To Pujan

To Sales

To Naveen

To Cash

| |

C

C

|

12,000

6,000

7,000

|

2,000

10,000

7,000

| 2011

Jan. 1

Jan. 3

Jan. 20

Jan. 21

Jan. 25

Jan. 30

Jan. 31 |

By Bal b/d

By Bank

By Salary

By Bank

By Shyam

By Interest

By Bal c/d | |

C

C

|

2,000

7,000

16,000

|

3,000

5,000

2,000

100

8,900

|

| | | |

25,000

|

19,000

| | | | |

25,000

|

19,000

|

2011

Feb. 1 |

To Bal b/d | |

|

16000

|

8900

|

| |

|

|

|

|

Note :

- Bank column debited as there is no information about Pujan's cheque.

- Transaction of Jan. 12 is related to credit sales hence not recorded in cash book.

- Cash column debited in transaction of Jan. 15 beacuse cheque has been deposited into bank at a later date.

PETTY CASH BOOK

Business has to incur small expenses which are repetitive in nature. To save the time and efforts of head cashier, business appoints a petty cashier. He is entrusted with the duty of paying these expenses.

IMPREST SYSTEM OF PETTY CASH BOOK

Under this system, Head cashier gives a fixed amount to petty cashier for a definite period. At the end of given period, Head cashier reimburses the amount actually spent by the petty cashier resulting the same amount with petty cashier which he had in the beginning of the period. This can be illustrated as under.

Illustrations 5: Prepare a Petty Cash book on the imprest system from The following transactions

| 2010 | | | | |

Amt (Rs.)

|

| Jan. 1 | Received from Head cashier |

500

|

| Jan. 2 | Bought stationery | | |

50

|

| Jan. 3 | Paid for registered post | |

30

|

| Jan. 4 | Bought Pen/Pencils for office use |

80

|

| Jan. 4 | Paid for Telegram | | |

60

|

| Jan. 5 | Paid for refreshment | | |

50

|

| Jan. 6 | Bought postal stamps | |

30

|

Solution :

Note :

- V.N. stands for Voucher number,

- The petty cashier can prepare different columns in "Analysis of Payments" as per his requirement depending upon the number of transactions.

SPECIAL PURPOSE SUBSIDIARY BOOKS

PURCHASES BOOK

In this book, only those transactions are recorded which are related to credit purchases of goods in which the business deals in. Recording is made on the basis of Bills/Invoice issued by the Suppliers.

Transactions not in purchases Book

- Purchases of goods for cash.

- Purchases of Assets meant for long term, not for resale purpose.

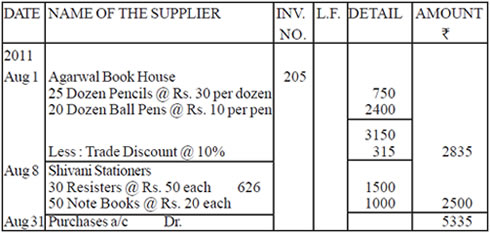

Illustration 5 : Enter the following transactions in the Purchases Book of M/s Ramesh Stationers :

| 2011 | |

| Aug 1 | Bought from Agarwal Book House (Invoice no. 205) 25 Dozen Pencils @ Rs. 30 per dozen 20 Dozen Ball pens @ Rs. 10 per pen Trade discount @ 10% |

| Aug 5 | Bought furniture of Rs. 20,000 on credit from M/s Interior Decor (Invoice no. 109) |

| Aug 8 | Shivani Bros. sold to us (Invoice no. 626) 30 Registers @ 50 each 50 Note Books @ Rs. 20 each |

| Aug 17 | Bought from Tushar stationers for (Cash memo no 101) 300 Refills @ Rs. 5 each 10 Ink pads @ Rs. 50 each |

Solution :

In the books of M/s Ramesh Stationers

PURCHASES BOOK

1. Tansaction of Aug. 5 is related to credit purchases of furniture i.e. an Asset.

2. On Aug. 17, goods bought for cash,

Hence both the transactions are not recorded in Purchases Book.

Advantages of Petty Cash book

- Saving of time and efforts of Head cashier

- Control on Petty expenses.

- Less chances of fraud.

SALES BOOK/SALES JOURNAL

In this book, transactions of credit sales of goods are recorded. The source document for this book is duplicate copy of invoice/bills issued to the customers.

Transactions not recorded in Sales Book

- Sales of goods for cash,

- Sales of Assets.

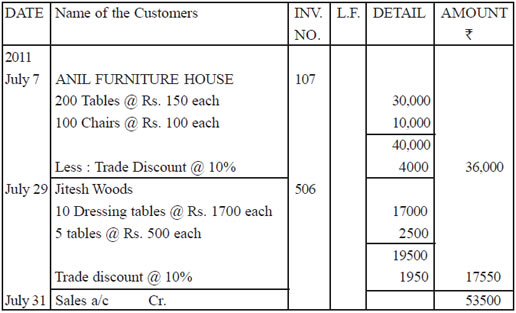

Illustration 6 : from the following transactions, Prepare a SALES BOOK of Alvin Furnitures:

| July 7 | Sold to Anil furniture house (Invoice no. 107) 200 Tables @ Rs. 150 each 100 Chairs @ Rs. 100 each Trade discount @ 10% |

| July 15 | Sold Air Conditioner to Ram Rs. 12000 |

| July 20 | Sold to Rama Furnitures (Cash Memo no. 3001) 10 Beds @ Rs. 2500 each |

| July 29 | Sold to Jitesh Woods (Invoice no.-506) 10 Dressing tables @ Rs. 1700 each 5 tables @ Rs. 500 each Trade Discount @ 10% |

Solution :

In the books of M/s Alvin furnitures

SALES BOOK

Note :

- Transaction of July 15 is related to sale of asset,

- Sale to Rama furnitures is made for cash,

hence not recorded in Sales Book.

PURCHASES RETURNS/ RETURNS OUTWARD BOOK

This book includes only those transactions which are related to returns of goods bought on credit. The goods may be returned due to various reasons such as goods bought being defective, supply of inferior quality goods etc.

Entries in this book are made on the basis of Debit Note. A debit note contains the name of the supplier to whom goods are being returned, details of goods returned.

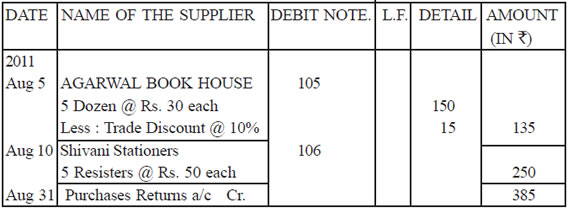

Illustration 7: Enter the following transactions in the Purchases returns book of Ramesh stationery house :

| 2011 | |

| Aug. 5 | Returned to Agarwal Book House (Debit note no. -105) 5 Dozen Pencils @ Rs. 30 per dozen Trade discount @ 10% |

| Aug. 10 | Returned to Shivani Bros. (Debit note no. 106) 5 Resisters @ Rs. 50 each |

Solution :

In the books of M/s Ramesh Stationers

PURCHASES RETURNS BOOK

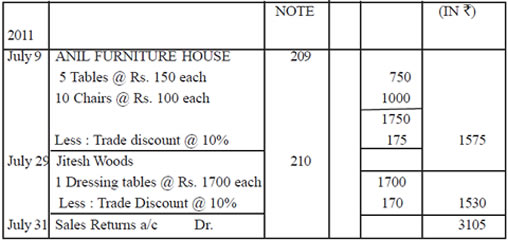

NOTE : Trade discount will be deducted if it was allowed at the time of purchase of goods.

SALES RETURNS BOOK

This book includes all the returns by customers of credit sales of goods. The Credit note is used for recording entries in this book. The credit note contains the details of Customers and goods returned.

Illustration 8: From the following transactions, Prepare a SALES RETURNS BOOK of furnitures :-

| Alvin | Furnitures :2011 |

| July 9 | Returned by Anil furniture house (Credit note no. 209) 5 Tables @ Rs. 150 each 10 Chairs @ Rs. 100 each Trade discount @ 10% |

| July 30 | Returned by Jitesh Woods (Credit note no. 210) 1 Dressing tables @ Rs. 1700 each Trade discount @ 10% |

Solution :

In the books of M/s Alvin furnitures

SALES RETURNS BOOK

BILLS RECEIVABLE BOOK

This book is prepared when bills receivable is a routine matter of business. A bill receivable is drawn by the seller of goods to the buyer and is returned by the buyer after accepting it. This book keeps the records of all the bill receivable and how it is being disposed by the firm.

FORMAT OF BILLS RECEIVABLE BOOK

Date of From Whom Received Period of Due L.F. Amount How of disposed

| Reciept | | the bill | date | | (In Rs.) | |

BILLS PAYABLE BOOK

This book keeps the records of all the bill payable that are accepted by the firm.

FORMAT OF BILLS PAYABLE BOOK

Date of

Accep-

tance | To Whom Given

| Period of

The bill

| Due

date

| L.F.

| Amount

(In Rs.)

| How disposed

|

JOURNAL PROPER

All those transactions, which can not be recorded in any of the subsidiary books mentioned above, are recorded in the journal proper or General journal.

The following types of transactions are recorded in this :-

1.

| Opening entries |

2.

| Closing entries |

3.

| Transfer entries |

4.

| Adjustment entries |

5.

| Rectifying entries |

6.

| Other entries |

No comments:

Post a Comment